2012 was a very tough year for global oil & gas, as the group underperformed the MSCI World by 10%. FTSE Oil & Gas was down 12% and SXEP down 4%.Starting with the disastrous performance of the US onshore-levered oil-field services stocks (the group was down 15% from the March peaks), sharp-sell off in US natural gas prices (-36% to the lows of $1.8/mcf only to end the year in the green) to profit-warnings from consensus top picks, we saw it all. Needless to say, dispersion of returns in 2012 was very high. Looking just at the top 25 oil & gas stocks by market capitalisation (>$40bn), which account for 55% of total global oil & gas market cap, performances range from -23% (Petrobras) to +42% (Ecopetrol). Continue reading Oil & Gas: Looking back at 2012… and a 2013 Outlook

Category Archives: Energy

Commodities Weekly

It was an uneventful week in crude markets. Continued delays in North Sea shipments continue to support Brent. However, OPEC production continued to slide in December, reaching a 0-month low. Cut in Saudi production is the main reason for the decline and was originally started to offset the gains in Libyan and Iraqi production. The decline is also in line with comments from Saudi oil minister and OPEC secretary general that the oil market remains well supplied. Continue reading Commodities Weekly

Egypt: A brief guide to the energy implications of the unrest

Here is a summary of my views on the Egypt crisis, stocks involved and how to play it.In terms of oil, none of the countries presently affected is a major producer in a global context of oil (1.1mb/d). Yemen and Egypt are important for gas markets as significant producers of LNG for international supply (20mtpa/ 8% global capacity). However, they are very important for low cost deliveries to Europe and for South Europe refiners (Repsol gets part of its crude for Cartagena and ENI for Toscana from Egypt).

Here is a summary of my views on the Egypt crisis, stocks involved and how to play it.In terms of oil, none of the countries presently affected is a major producer in a global context of oil (1.1mb/d). Yemen and Egypt are important for gas markets as significant producers of LNG for international supply (20mtpa/ 8% global capacity). However, they are very important for low cost deliveries to Europe and for South Europe refiners (Repsol gets part of its crude for Cartagena and ENI for Toscana from Egypt).

The threat of contagion within the MENA region (Algeria, Bahrain, Djibouti, Egypt, Iran, Iraq, Jordan, Kuwait, Lebanon, Libya, Morocco, Oman, Palestinian territories, Qatar, Saudi Arabia, Ethiopia, Sudan, Syria, Tunisia, United Arab Emirates and Yemen) is what most analysts see as most worrying. I would categorize the risk as low in the pure arab states (Saudi-EUA-Kuwait and Iran) and higher in Algeria, Jordan and Syria, where civil unrest has been highest (food prices up 59% in Jordan and Syria while unemployment soared). Out of these, only Algeria is a serious threat to global supply of gas.

Algeria has 159 trillion cubic feet (Tcf) of proven natural gas reserves – the tenth-largest natural gas reserves in the world, and the second largest in Africa. Algeria produced 3.08 Tcf of dry natural gas in 2010, and consumed 1 Tcf of dry natural gas domestically.

Egypt consumed more than it produced for the first time in 40 years in 2010.

Egypt’s EGPC is a strange animal as it does not operate any of the licenses in the country, but foresees the developments and takes the money. Most of the production is offshore or in the Western desert and has not been affected by the riots. As an example, in the past 20 years of presence of Apache in the country there has never been a change of license or nationalization. Egypt also has a very advantageous (for the country) taxation system, local content employment requirements and now that is a net importer, needs more from IOCs than ever.

The final risk is the possibility of disruption to the smooth passing of ships through the Suez Canal. So far this has been denied as a threat.

Companies exposed to Egypt and Algeria.

If we establish the low(er) risk of disruptions in Saudi, Iran, Iraq, etc… The key companies exposed to the Egypt problems are:

OMV, REPSOL & ENI have the largest exposure with c.20% of their commercial reserves in the region.

ENI’s Egyptian exposure is 14% of group production and 7% of upstream value. However, ENI is the most exposed to North Africa and the MENA with additional risk to supplies to Italy from Egypt and Algeria. Eni has a limited exposure to Egypt but 36% to the region (including Libya and Algeria).

OMV has a 20% exposure to the region (mainly Lybia) and recently added exposure to Tunisia through an acquisition. OMV, Total and BP each gets 3-4% of their total production from Tunisia, Egypt and the Yemen in aggregate. However, Egypt, Tunisia and Yemen account for quite more than that in their growth strategy and give them the highest ROCE. Exxon also drills offshore Egypt but the exposure is negligible. Chevron and Conoco also only marginally present. Of the rest, exposure is also quite small, including Statoil with less than 10% upstream value exposure (mainly Algeria).

BG. Egypt and to a lesser extent Tunisia are relevant production centres with around 30% or 220kboe/d of its 2009 production. Worth noting it is mostly offshore, with a large presence of local workforce and that there has been no disruption to activities.

GDF-Suez, Shell. Jointly operate the Alam El Shawish concession in the western desert area of Egypt. In Egypt, GDF Suez holds stakes in two other offshore licenses: it operates and owns 50% in West El Burullus area (together with Dana Petroleum, bought by KNOC), where an initial discovery was announced in 2008 and has 10% in the North West Damietta licence operated by Shell (61%). In liquefaction gas, GDF owns 5% in the first LNG train from the Idku plant that delivers 4.8 bcm of natural gas annually and buys its total production. GDF SUEZ loads about 60 cargoes per year.

Gas Natural-Fenosa, Repsol YPF. Gas Natural owns and operates the Egypt Damietta liquefaction plant. The Egyptian government told Gas Nat-Fenosa to consider importing gas from abroad to meet the needs of the Damietta liquefaction unit located on the Egyptian Mediterranean coast, after the company suffered from a set back in its supplies from the gas national network during the first half of the fiscal year 2009/2010. The firm currently receives 320 million cubic feet of gas per day, 70% of it from the Egyptian Natural Gas Holding Company (EGAS).60% of natural gas delivered to Spain comes from Sonatrach (Algeria). Risks have increased in an ongoing and well-known dispute between the countries. Gas Natural lost the license for Gassi Touil in 2009.

RWE. In recent years the company made a number of major gas discoveries in Egypt and boosted its activities considerably with the acquisition of additional concessions. RWE Dea has a total of 13 onshore and offshore concessions in Egypt, across a concession area of about 13,300 square kilometres in the Nile Delta, Gulf of Suez and Western Desert.

EDF through Edison (Italy) Holds the $1.4-billion concession agreement for the offshore fields of Abu Qir, which has lost them money and were trying to sell or renegotiate.

Apache. Egypt is 21% of Apache’s production. Most of their assets are in the Western Desert. Apache is critical to Egypt as it drills 50% of all the country wells, supplies gas domestically at prices that are 60% below international prices, and employs 5000 Egyptians. Apache pays $11m a day in taxes to the treasury.

Premier has a very small exposure to Egypt (only 20% stake in a non-operated field).

Of services, Halliburton and Schlumberger undertake around 70% of the oil and gas service contracts in Egypt. Transocean has 10 jack-up rigs in Egypt, more than any other company, although six of those rigs are either cold-stacked or idle. Diamond Offshore has 3 rigs, 8% of its total rig count. Rowan Companies has 1 rig, but it wasn’t in use as of this week. Petrofac had a contract in Egypt that finished in December, and has no further exposure to Egypt but is very exposed to MENA region (15-20% of backlog). Saipem and Technip also have c20% of backlog in the region.

The biggest threat in my view is to the big IOCs and utilities who tend to solve these issues through paying up, and losing returns.

Play the oil and gas spike through utilities (generators with no Egyptian MENA exposure) and high oil geared explorers and producers more exposed to LatAm, US and especially Russia. Gazprom will love this MENA problem.

I see services relatively unaffected once the risk of oil and gas field shutdowns is clarified. In the Iraq war and other risky geopolitical environments the specialized names benefited from the need to protect and continue operating the oil and gas fields. However, the short term impact will likely continue to be negative. This is also bad for southern european refiners because their low cost oil comes from Lybia and Egypt and the refining margins will likely fall as oil rockets but heavy-Brent spreads collapse.

Further read:

http://energyandmoney.blogspot.com/2011/03/war-in-lybia-and-possible-algerian.html

http://energyandmoney.blogspot.com/2011/02/lybia-in-flames-and-clash-of.html

http://energyandmoney.blogspot.com/2009/11/china-exxon-and-war-for-resources.html

Continue reading Egypt: A brief guide to the energy implications of the unrest

Some energy thoughts for 2011

(This article was published in Spanish in Cotizalia on December 23rd 2010)

First of all, dear friends,I wish you all a 2011 filled with peace and prosperity.

As this is a time of predictions, and last year I was not very wrong, I’d like to leave my humble opinion on what 2011 can bring us, I see as a year of consolidation of trends in 2010: OECD decline up to their eyeballs in debt, low rates and more inflationary monetary policies.

. Oil at $105/bbl due to increased emerging market demand . With +1.5 to 2% oil demand growth in 2011, 75% from emerging markets, crude oil inventories should be reduced to levels close to the average of the last 5 years. Global demand will continue to be dominated by growth in China, India, Latin America and the producer countries. Pay attention to demand. It’s all that is going to move prices. Do not bet on peak oil theories or supply shortages in 2011. OPEC still has 5 million barrels per day of spare capacity, and we will see Russia confirming its 10.2mbpd output, while Saudi Arabia could easily increase production by 1mmbpd if needed. The world economy has shown that oil at current prices is not a problem. A high price is a sign that the economy works, companies are investing more in exploration, they discover more and the total cost to consumers does not rise due to crude prices, but due to taxes. The cost of fuel is less than 25% of the cost of airlines, and a tiny percentage of the final price of petrol and diesel (55% -60% is tax).

We have oil for many decades. More than sixty years of demand in proven reserves. And rising. In 2010 the replacement rate of global reserves will exceed 100%. And with a 17% increase in overall investment in exploration and production, the chances of a global reserve replacement of 100% in 2011 are very high. And probably in the coming months we will see major innovations in unconventional oil, as we saw in shale gas. If oil stays above $60/bl, as expected, investments in new unconventional reserves, which rose 230% in the past five years, will continue to grow.

Bad year ahead for Iraq and Nigeria. The price of oil is not flowing to the people and patience is being exhausted. We are seeing new security problems in the Niger Delta, and I think in 2011 we will have some major scares. In Iraq, the war is now administrative. On a recent visit to Baghdad by a group of investors, companies made it clear. With no stable government, no legal clarity and security to invest, it is impossible to reach 3-3.5 million barrels per day of production. Beware of listed exploration companies heavily exposed to Iraq especially those that rely to Kurdistan to work.

I still see a positive environment for service companies that benefit from increased investment, from Petrofac and Seadrill to downstream-heavy TRE. I am still cautious on seismic names. Capacity is way too high and increasing, while demand has not recovered to absorb the already high supply, so margins are not going to rise easily. As for independent exploration and production companies, the war for natural resources will accelerate M&A, and growth new frontiers. Focus on Tullow, Soco, Chariot, OGX, Cairn, Anadarko and Novatek.

M&A in Oil & Gas will surpass the $150bn mark set in 2010. Large companies have to find truly transformational deals to drive growth that has been so elusive in 2000-2010. More shale gas ventures in the US can be expected, but I believe the focus will be in frontier areas: West Africa and LatAm.

Refining margins are likely to do nothing as the economy recovers but overcapacity continues to dominate the refining sector. We had 7mmbpd of overcapacity and this is rising, with 370 refining projects in 90 countries around the world in the next five years (UBS source).

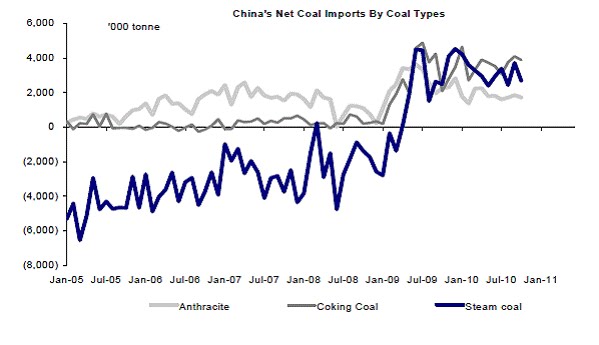

. Coal, Coal, Coal. Coal at $140/MT. China burns 55% of the world’s coal, and that number is expected to rise by 65% over the next five years. China has half the U.S. GDP and consumes 3 to 5 times as much coal. And in India and the rest of Asia the situation is similar. Despite the environmental rhetoric that we use, these countries do not have to cut their growth just because we say so. Meanwhile, the supply problems will continue, with the protests of organized groups in Newcastle and flooding problems in Australia. As of today, c.100mMt of annual coking coal production (c.40% of the global supply) is under force majeure arrangements.

. Weakness of carbon dioxide (CO2). You know it, that “fake commodity” artificially invented, where demand and supply are imposed by political entities… and it still does not work. In 2010, CO2 has barely kept the €14/MT level. Neither Copenhagen, or Cancun, or the efforts of several investment banks and environmentalists have helped to raise the price. The alarms bells are ringing and there are voices calling for imposing a minimum price for CO2. Interesting. The interventionists were rubbing their hands at the prospect of increasing the price of CO2 through more than questionable environmental policies, and now they need to find inflation through imposition.

The supply of CO2 (EUAs) exceeded 24.8mMt in November (a record) and 24.4mMt in December. With the European Union and OECD undergoing a very slow recovery in 2011 and the most environmentally committed countries experiencing huge debt problems with c$300 billion to refinance in 2011, the excess supply will increase.

The companies benefited in this environment may be the traditional power generators.

Beware of turbine manufacturers. 2010 was no exception, it was the the beginning and the fall in new installations will continue impacting a sector with significant overcapacity. Europe new installations will be flat at best, China up 10%, US flat at best, rest of the world +5%, driving a +5% to +13% growth in the global market… while manufacturing capacity, which was already too high, has increased by c8%, driving a 39% oversupply (MAKE, GWEC source).

. Natural Gas to suffer for another couple of years. A bad nat gas year is one that sees the price of Henry Hub at $4.5/MMBTU amid the coldest winter of the last ten years. In 2011 we will continue in a complex environment. Liquefaction capacity increasing by 10BCM, shale gas production increasing by 6% and a very slow recovery in demand for electricity. The NBP (UK) price will continue to support the $7/MMBTU equivalent thanks to the decisions of Qatar, Norway and Russia to control supply. The liquefied natural gas sold to Asia will continue to trade at a premium over Europe, but a significantly lower one, as supply problems in Korea, Japan and China are eased.

Of course, a volatile gas market benefits the companies that profit from arbitrage between markets, like BG Group, but also to a lesser extent, Statoil and Shell. The losers are still the Central European power conglomerates heavily exposed to gas, and companies like Gazprom, which will again have to renegotiate some contracts.

. The nuclear renaissance is delayed, but it is happening. Low power prices, weak gas and excess capacity have delayed plans in the UK and other European countries to increase their nuclear fleet. But if they care about the environment and strive to reduce CO2 emissions, the nuclear option is the only real alternative to achieve these goals. The nuclear renaissance is inevitable in China, Russia and other countries. 56 reactors under construction, 20 of them between China and Taiwan. More than 180 gigawatts of new nuclear capacity through 2024.

The winners in this environment are the equipment companies that build new plants, Siemens, Alstom and Amec. Nuclear-heavy generator stocks are more dependent on the evolution of power prices. And in that area, in 2011, again we will see major differences between countries with capacity problems (Nordpool, with hydro reservoirs at 24%) and over-capacity countries (Germany, Spain, Italy). In Europe power demand growth in 2010 (+3.5%) did not offset the fall of 2009, while capacity continued to increase (predominantly solar and wind). This is not a positive backdrop for power prices throughout the continent.

Further read:

http://energyandmoney.blogspot.com/2010/01/energy-predictions-for-2010.html