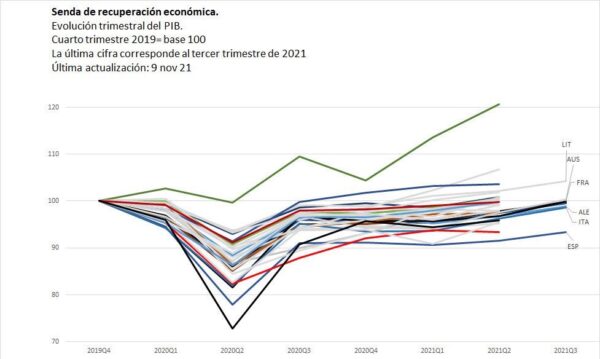

The global recovery has slowed down significantly since the peak of the re-opening effect in June 2021. What many expected would be a multi-year cycle of above-trend growth is proving to be a more modest bounce. Furthermore, according to Bloomberg Economics, the global economy will likely grow in the next ten years at a slower pace than in the decade prior to the pandemic.

Continue reading 2022, The Year of The Hangover?All posts by Daniel Lacalle

The Fed’s Dovish “Tapering” And The ECB

This week, the Federal Reserve gave the most dovish “hawkish” statement ever. An apparent aggressive tapering that, in reality, means maintaining very low rates and massive repurchases for longer.

Inflation has skyrocketed and aggressive monetary policy is the key factor in understanding it. I already explained it in my article “The Myth of Cost-Push Inflation”. The Federal Reserve has finally recognized this and has made a U-turn in its policy of maintaining stimulus despite inflationary pressures.

The Federal Reserve now expects core inflation to remain above 2.7% in 2022 (previously it expected 2.3%) and that it will be above 2% in 2023 and 2024. That means the CPI (Consumer Price Index) will probably remain above 3-4% in that period. Taking into account that it will close the year above 6%, we are talking about an accumulated inflation of more than 14% in three years, a great risk for the recovery, real wages, family savings and investment.

Continue reading The Fed’s Dovish “Tapering” And The ECBThe Myth Of Cost-Push Inflation

Senator Elizabeth Warren recently stated that rising prices were due to corporations increasing their profits. “This isn’t about inflation, this is about price gouging for these guys”. It is simply incorrect.

No, corporations have not doubled their profits, and rising prices are not due to the evil doings of businesses. If evil corporations are to blame for rising prices in 2021, as Elizabeth Warren says, I imagine that they were magnanimous and generous corporations when there was low or no inflation, right?

Inflation is the tax of the poor. It destroys the purchasing power of wages and engulfs the little savings that workers accumulate. The rich can protect themselves by investing in real assets, real estate and financial, the poor cannot.

Continue reading The Myth Of Cost-Push InflationSpain’s Fake November “Employment Boom”

The Spanish government and its supporters question the GDP figures, which show a very poor recovery, lagging behind the OECD and European Union, stating that employment is recovering stronger therefore the GDP figure must be wrong.